Most investors default to cash when uncertainty rises. Reducing exposure and holding liquidity feels like the disciplined choice. Sometimes it is. But it is rarely the best way to protect capital over a full market cycle.

Cash carries a cost that rarely shows up on the same timeline as the comfort it provides. A portfolio that moved to 30% cash in early 2020 avoided much of the S&P 500's 34% drawdown between February 19 and March 23 of that year. It also missed much of the recovery. The index surged roughly 60% from its March low by November 2020, and the compounding that followed widened the performance gap for years afterward.

The real question for family offices, endowments, foundations, and UHNW individuals managing significant capital is not whether to take risk or avoid it. It is how to structure a portfolio that manages downside exposure without sacrificing the market participation that compounds wealth over time.

IN BRIEF

Protecting capital while staying invested requires structural tools — including dynamic position sizing, selective hedging, long/short flexibility, and leadership-quality screening — rather than the binary choice between full exposure and cash. The cost of cash is measured in missed compounding, which accumulates over time in ways that are rarely visible until years after the decision to step aside.

Why is cash a more expensive hedge than it appears?

The case for holding cash during uncertainty seems straightforward: preserve capital, reduce volatility, wait for clarity. But this framing treats risk as a single variable, the chance of loss. In practice, risk has two dimensions: the risk of losing capital and the risk of failing to grow it.

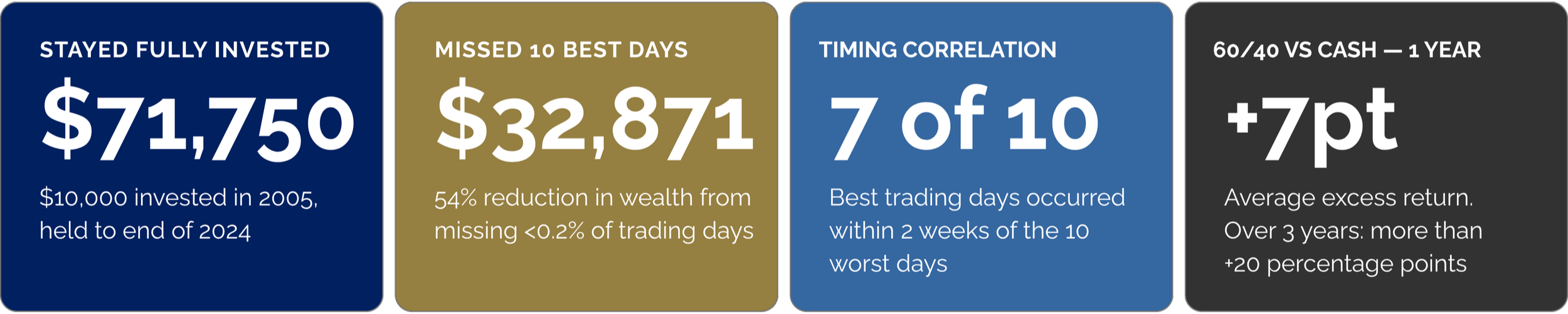

The numbers illustrate a structural problem, not just a timing risk. Seven of the 10 best trading days over that period occurred within two weeks of the 10 worst days. Stepping out to avoid the worst days almost guarantees missing the best ones. The implication for portfolio construction is that capital protection strategies built around exiting and re-entering the market face a structural disadvantage that compounds over time.

A 60/40 portfolio of equities and government bonds has outperformed cash more than 70% of the time over any one-year horizon and in the vast majority of rolling three-year periods, with average excess returns above cash of 7 percentage points over one year and more than 20 percentage points over three years, according to JPMorgan research.

For family offices managing multigenerational wealth, endowments supporting annual distributions, and foundations funding ongoing programs, missed compounding is the more consequential risk. The question becomes practical: how do you reduce downside exposure without giving up the market participation that produces long-term returns?

What behavioral patterns typically undermine capital protection efforts?

Understanding these tools is necessary. Applying them when markets are falling sharply is harder. Three behavioral patterns tend to undermine capital protection, and each carries a hidden cost:

How capital protection connects to long-term portfolio construction

Capital protection is about maintaining a portfolio structure that can absorb setbacks, act on opportunities, and compound capital through full market cycles.

What makes an investment strategy durable over time is the same set of structural disciplines that protect capital in the short term: dynamic sizing, selective hedging, leadership screening, and the analytical framework to distinguish temporary price declines from genuine deterioration. Applied consistently, not reactively.

For family offices, endowments, and foundations evaluating how to allocate capital in uncertain markets, the structural approach to protection is more reliable than the timing approach. The investors who have historically preserved and grown capital through volatile periods were not the ones who predicted market direction correctly. They were the ones whose portfolio structure could absorb the surprises they did not predict.

We assess leadership quality,

capital allocation discipline,

and decision-making patterns

We build portfolio structures around those assessments that protect capital without requiring us to predict market direction. If you're thinking about how to structure your portfolio for protection and participation, we're always open to a thoughtful conversation.

Schedule a Confidential DiscussionCash eliminates the first and guarantees the second.

JPMorgan Asset Management's Guide to the Markets, one of the most widely referenced datasets in institutional investing, tracks what happens to a hypothetical $10,000 investment in the S&P 500 depending on whether the investor stays fully invested or misses the strongest recovery days. Their data shows that $10,000 invested in 2005 would have grown to approximately $71,750 by the end of 2024 if the investor stayed fully invested. Missing just the 10 best trading days over that period would have cut the ending value to roughly $32,871. That is a 54% reduction in total accumulated wealth from missing fewer than 0.2% of trading days. Missing the best 60 days would have left the investor with less than the original $10,000.

How is capital protection structured without liquidating positions?

Protecting capital while staying invested is a structural challenge, not a timing decision. The following mechanisms work together to reduce downside exposure while maintaining the portfolio's ability to participate in rising markets. What ties them together is the same discipline: each one replaces a reactive, emotion-driven decision with a pre-built analytical framework.

Which signals should shape portfolio exposure decisions?

Rather than watching market direction, we focus on signals that indicate when and how to adjust exposure: