Andy Jassy Didn't Just Report a Number. He Settled a Debate

Andy Jassy Didn't Just Report a Number. He Settled a Debate.

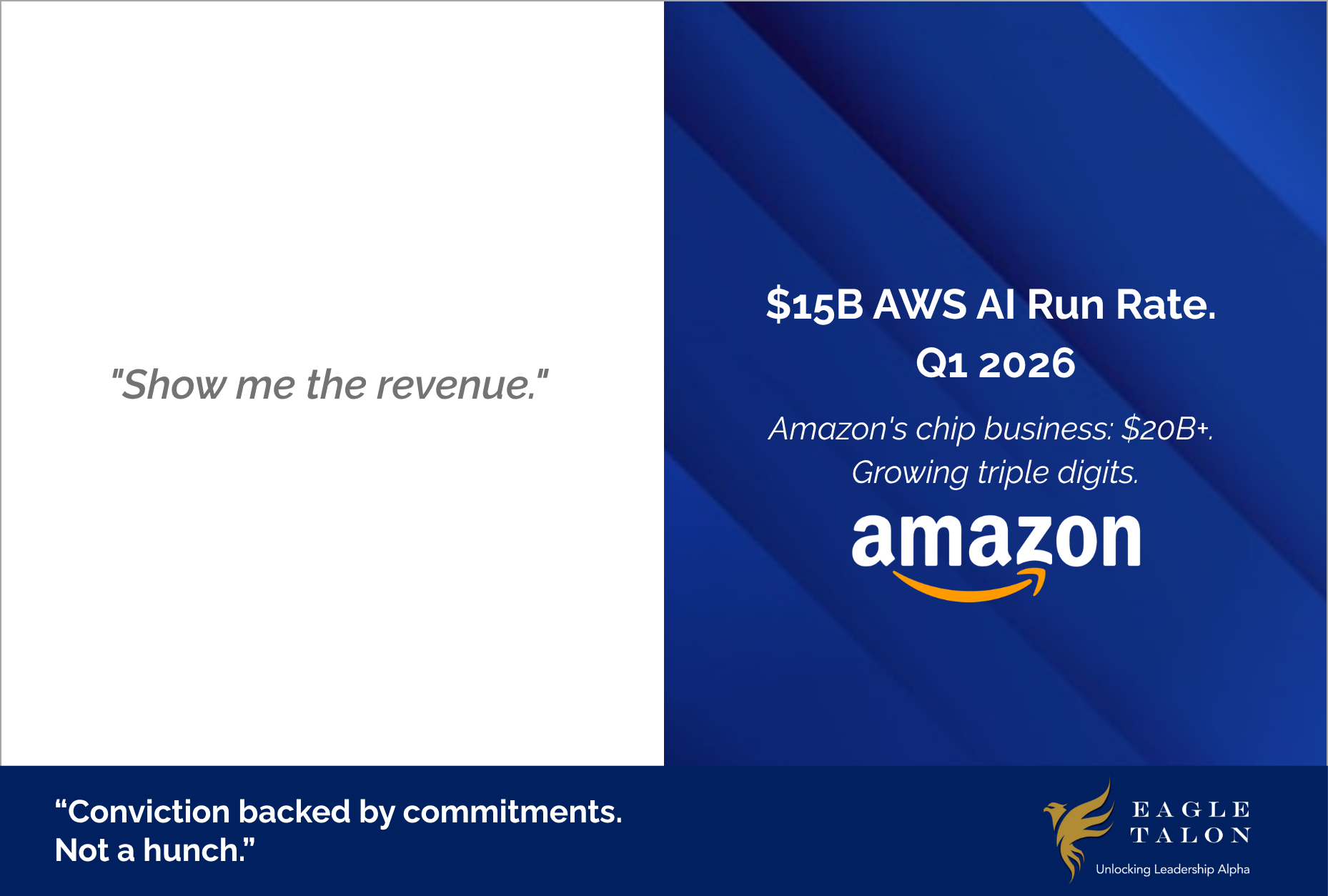

For two years, the loudest criticism of big tech's AI spending has been the same. Show me the revenue.

Jassy answered that recently.

Three years into the AI wave, AWS AI revenue is running at over a $15 billion annual run-rate as of Q1 2026, the first time Amazon has disclosed this figure publicly. That's roughly 10% of AWS's entire $142 billion revenue run rate.

Sequentially, Amazon's custom chip business, Graviton, Trainium, and Nitro, has surged to over $20 billion in annualized revenue, doubling from the $10 billion disclosed just last quarter and growing triple digits year over year.

The stock rose roughly 5% on the news. Not on hype. On proof.

Here's what the market is actually pricing in now:

➤ Jassy committed approximately $200 billion in 2026 capex and disclosed that customer commitments already cover a substantial portion of it, with much of that spend expected to be monetized in 2027 and 2028

➤ Capacity is the constraint, not demand. AWS would be growing faster if they could build faster

➤ Two customers asked to buy all of Amazon's available Graviton chip capacity for 2026 — committed demand, fully subscribed, ahead of broad availability

At Eagle Talon, when a CEO publishes numbers this specific in a shareholder letter, we revisit our investment thesis.

Because the signal here isn't just growth in AI revenue. Jassy's confidence is backed by customer commitments, not forecasts.

He's investing $200 billion because the demand is already there — and the cloud and chip infrastructure to capture that revenue is still being built.

That opportunity is why investors are now asking: which companies are turning AI spend into actual revenue, and which ones are still answering what Jassy has now put to rest?

Which companies do you see turning AI capex into durable, measurable returns?

🔗 Source: 'Not on a Hunch': Andy Jassy Defends Amazon's $200B Spending Spree