The ten largest companies in the S&P 500 now represent over 40% of the index — nearly double their weight a decade ago. A portfolio that holds a broad index fund and calls itself diversified may be placing an outsized bet on the capital allocation decisions of fewer than a dozen CEOs.

That concentration has been rewarded recently. But the same mechanism that amplifies returns on the way up tends to amplify losses when the drivers shift. When a handful of leadership teams are responsible for that much of the index, the quality of those leaders' decisions becomes a portfolio-level risk factor. Most family offices, endowments, and foundations are not explicitly managing for it.

IN BRIEF

Market concentration risk is the vulnerability that builds when a small number of companies drive the majority of an index's returns. Portfolios that appear diversified through broad index exposure may carry hidden dependence on the leadership decisions and capital allocation discipline of a narrow group of businesses. When confidence in those leaders changes, concentration doesn't unwind gradually. It reprices quickly.

How concentrated are indices right now?

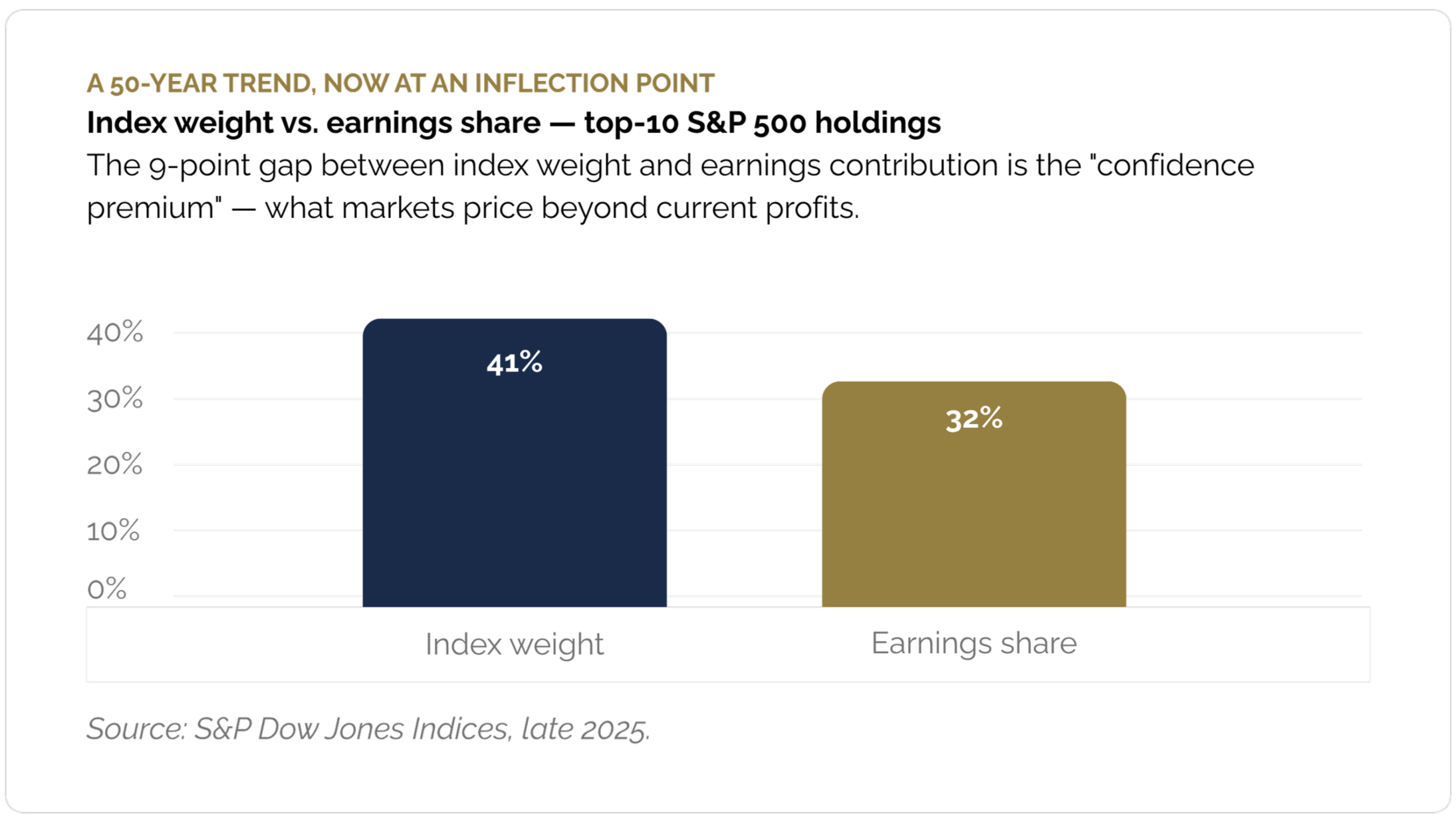

As of late 2025, the top 10 stocks in the S&P 500 accounted for approximately 41% of the index's total market capitalization, according to data from S&P Dow Jones Indices. That is the highest concentration on record. The prior peaks, in 1980 and at the height of the 2000 technology bubble, saw the top 10 reach roughly 26%. Current levels exceed those historical extremes by a wide margin.

Those top 10 companies represented roughly 41% of the index's weight but were expected to generate only about 32% of its earnings. That gap measures something specific: a portion of the premium investors are paying reflects confidence in future growth and continued dominance, not current profitability.

For family offices, endowments, and foundations that allocate through index funds or market-cap-weighted strategies, this creates an exposure that may not match their intent. A family office that believes it holds broadly diversified public equity exposure may actually have close to half its capital dependent on the continued execution of a small number of leadership teams.

What drives concentration, and why the source matters

Not all concentration carries the same risk. We think about it through three distinct layers. The question that matters most is which layer is driving the valuation premium at any given moment.

Structural concentration is driven by index construction rules and passive capital flows. As index funds have grown, capital has flowed through ETFs and passive vehicles into the largest companies regardless of valuation or fundamentals — creating self-reinforcing momentum.

Fundamental concentration is supported by genuine earnings strength. When the largest companies are also the most profitable — generating strong revenue growth, high margins, and superior returns on capital — concentration has an earnings foundation. This is the most defensible form.

Leadership-driven concentration reflects market confidence in specific management teams: their strategic vision, their capital allocation track record, and their ability to sustain competitive advantages. This layer is the most fragile. Confidence in leadership can shift faster than either index mechanics or earnings fundamentals.

Why leadership quality carries outsized consequences

When a handful of companies drive index returns, leadership decisions at those companies carry consequences far beyond the individual stock. A single capital allocation mistake by a CEO whose company represents 5% or more of the S&P 500 doesn't stay contained. It flows through index returns, through passive fund performance, and ultimately through every portfolio that relies on market-cap-weighted indices.

Hendrik Bessembinder's research at Arizona State University reinforces how concentrated value creation has always been: just 2% of publicly listed companies produced 90% of the $79.4 trillion in aggregate shareholder wealth creation between 1926 and 2024.

Three signals Eagle Talon monitors

Capital allocation discipline under scrutiny. Are the largest companies deploying capital toward their highest-return opportunities, or are they spending to defend market position? For several of the largest S&P 500 constituents, annual capital spending now exceeds $50 billion. Whether that capital earns an adequate return over the next three to five years will likely determine whether current concentration levels are sustainable.

Strategic consistency versus narrative shift. Leaders under short-term market pressure sometimes shift strategy in ways that are difficult to detect in real time. A company that built its valuation on one competitive advantage but begins spending heavily on an adjacent opportunity may be adapting intelligently — or drifting from the economic model that justified its premium.

Execution patterns and decision tempo. Isolated operational issues are noise. Recurring ones — missed product launches, integration failures, organizational restructurings — suggest the leadership quality behind the valuation may not match the confidence the market is pricing.

Concentration exposure is a leadership evaluation problem

— not just a portfolio construction one.

When a handful of companies drive index returns, assessing who runs those companies and how they allocate capital becomes a core part of portfolio risk management.

Eagle Talon Partners evaluates market concentration through the lens of leadership quality, capital allocation discipline, and decision-making patterns.

What to watch: early signals of a concentration shift

Shifts in concentration dynamics tend to surface well before reported financials reflect them. Four areas deserve attention:

MONITORING FRAMEWORK

Four early-warning signals

These signals typically surface before the financials confirm them. Monitor quarterly.

How investors should think about concentration in portfolio construction

The response to market concentration risk is not to avoid the largest companies. Many of them are genuinely exceptional businesses with strong leadership and defensible competitive positions. The response is to ensure that concentration exposure is deliberate and informed, not accidental.

That means three things in practice. First, explicitly measuring how much of the portfolio's return depends on a narrow set of companies and their leadership teams. Second, assessing whether the concentration is justified by current earnings and capital allocation quality or inflated by structural flows. Third, maintaining enough portfolio flexibility to adjust if the leadership signals at the most heavily weighted positions begin to deteriorate.

For family offices, endowments, and foundations with a long time horizon, the ability to evaluate leadership quality at these positions is particularly important.

We evaluate concentration through

the lens of leadership quality

Eagle Talon Partners identifies whether the confidence driving the most heavily weighted index positions is warranted by the quality of the leaders behind them. If you're thinking about how concentration risk fits into your portfolio strategy, we're always open to a thoughtful conversation.

Schedule a Confidential Discussion