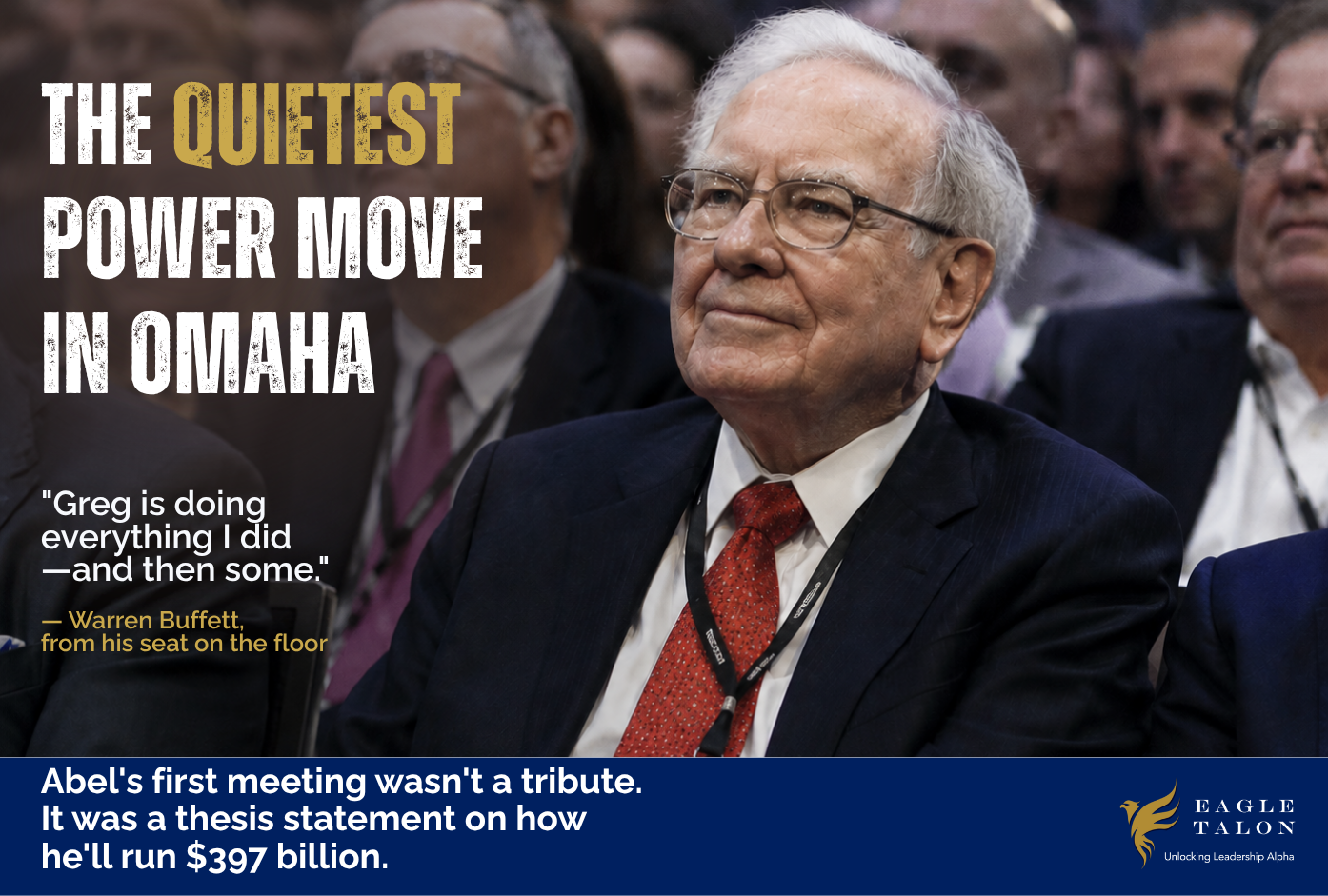

Greg Abel's first annual meeting could have been a tribute. It was an operational audit

Greg Abel's first annual meeting could have been a tribute. It was an operational audit.

He opened with a near-hour walk through every major Berkshire business. Railroad. Insurance. Energy. Retail. Segment by segment, challenge by challenge. Shareholders came expecting nostalgia. They got a CEO who chose substance over sentiment.

The Q1 numbers supported him. $11.35 billion in operating earnings. Insurance underwriting profit up 29%. Cash swelled to $397 billion from $373 billion at year-end. Buybacks resumed.

Most successors spend the first year performing a version of their predecessor. They borrow the language, adopt the habits, defer to the legacy. Abel showed up as himself: operational, precise, deeply knowledgeable. He let the results speak.

Buffett said it from the front row: "Greg is doing everything I did and then some, and he's doing it better in all cases."

Q2 earnings land August 3. But the more consequential test may be what Abel does with $397 billion in cash. Buffett's discipline was to wait for the right opportunity at the right price.

If Abel deploys at scale in the next two quarters without a clear margin of safety, that signals the acquisition discipline has changed. If he holds, it confirms the framework survived the founder.

At Eagle Talon, we evaluate leadership transitions by a single question. Does the successor preserve the capital allocation discipline that built the franchise, or break from it? Abel's first five months point toward preservation. The open question is whether that holds when a large, actionable deal surfaces.

What would change your read on Abel: the Q2 earnings, or how he handles the first acquisition-sized opportunity?